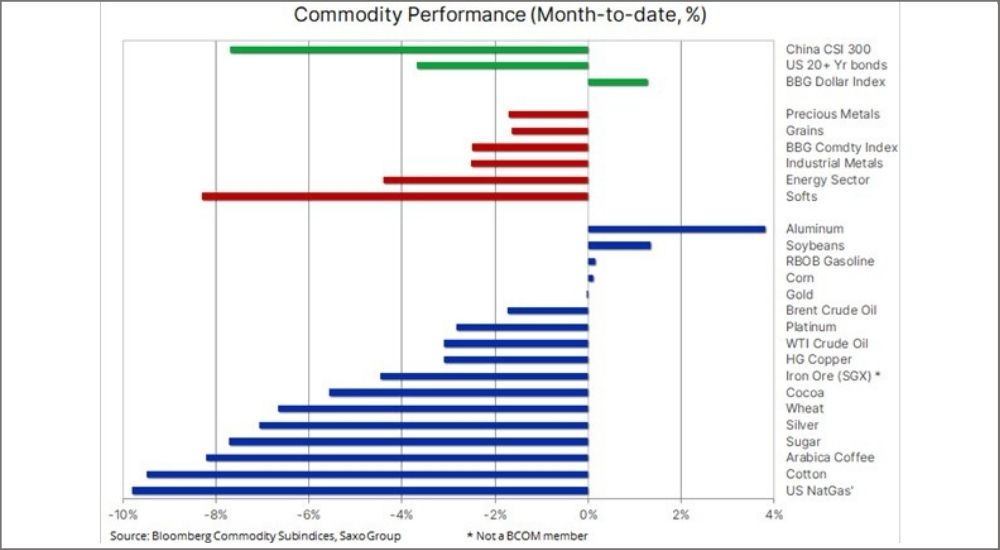

Bloomberg Commodity records weakest month since Sep 2020 impacted by Chinese slow down, lockdowns

The Bloomberg Commodity index, currently down 2.3% on the month, is on track to record its weakest month since last September. A weak sentiment in Asia has taken over as a factor supporting the dollar thereby driving consolidation in a widening number of commodity prices, most lately industrial metals.

Adding to the current loss of momentum has been the surge in US treasury yields, lockdown extensions and vaccine hiccups in Europe as well as signs that China has begun scaling back its massive stimulus program which supported both the Chinese and the global economy during the early stages of the year-long pandemic.

In Q2, we still look for the US dollar to turn back lower, but tactically there is considerable room for a rally extension as long as US growth prospects are seen as leaps and bounds beyond most of the rest of the world and as long as the Fed ignores the longer term impossible math of incoming treasury issuance later this year (and with an eventual Biden multi-trillion dollar infrastructure plan) relative to the current scale of Fed QE purchases.

Copper is trading below local support at $4/lb, but has so far managed to find pockets of buying interest ahead of $3.93/lb, the 50% retracement of the run up since late January. While the long-term outlook for copper remains solidly bullish, due to signs of structural supply tightness, the market has lost momentum in response to an 80% bounce in exchange-monitored inventories in London, Shanghai and New York.

While managing to trade sideways since the end of the Chinese New Year, the sentiment has been weakening amid signs of weakness in China where the scaling back of stimulus has been seen as one of the reasons behind the 18% drop in the CSI 300 during the past five weeks. Speculators meanwhile have been net-sellers of High Grade copper for the past four weeks which has brought the net long down to just 45k lots, an eight month low.

With this in mind there is a risk that continued liquidation of weak longs could see it retrace lower towards $3.88, the 50-day moving average, a level where tactical longs are likely to emerge with a stop below $3.80.

The weakness in industrial metals has added another headache for silver which has struggled this past week, and the break below $25 today has seen its relative value against gold drop to a two-month low with the XAUXAG ratio trading back above 70 ounces of silver to one ounce of gold. In the process it has fully retraced the crazy and non-fact based silver squeeze that briefly took it above $30 on February 1.

Overall, silver remains stuck in a very wide $22.50 to $30 range but given its high beta and the risk of continued dollar strength, the metal is risking another speculative clearance before eventually, which we believe it will, finds renewed support.

Finally, US growers may plant their largest area since 2014 this coming summer. During the past year the Bloomberg Grains index has jumped by more than one-third with soybeans (+58%) and corn (+45%) trading at their highest levels in more than seven years. While it may take 5-10 years for mining companies to raise production in response to higher prices, farmers can respond from one year to the next. The US Department of Agriculture will release its plantings outlook on March 31, and weather permitting, a bumper crop is expected with surveys pointing to increased acreage allocation for soybeans and especially corn. Speculators hold a near record long so expect increased volatility before and after the release.